Giant silver and antimony project commences trading in the USA: (OTCQX: SSLVF)

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 3,300,752 SSLVF/SS1 Shares at the time of publishing this article. The Company has been engaged by SSLVF/SS1 to share our commentary on the progress of our Investment in SSLVF/SS1 over time. This information is general in nature about a speculative investment and does not constitute personal advice. It does not consider your objectives, financial situation, or needs.

One of the largest pre production silver mining projects located in the USA just commenced public trading…

in the USA.

The code is OTC: SSLVF

The name is Sun Silver.

SSLVF has a 480M oz silver equivalent resource in Nevada

It also contains critical military metal antimony…

(antimony is critical for making bullets, missiles, tanks and all sorts of important military uses but the USA has zero domestic supply)

Silver and antimony prices are both at record highs.

Both silver and antimony have been declared as “critical metals” by the USA.

…and 7 days ago China declared NEW tighter rules on exporting both silver and antimony:

(source - official statement (Chinese) , English translation, Chinese English language media, US based media coverage)

A good time to build a USA based silver and antimony mine…

Our 2024 Small Cap Pick of the Year Sun Silver (ASX: SS1, OTC: SSLVF) owns one of the largest pre-production silver assets in the USA.

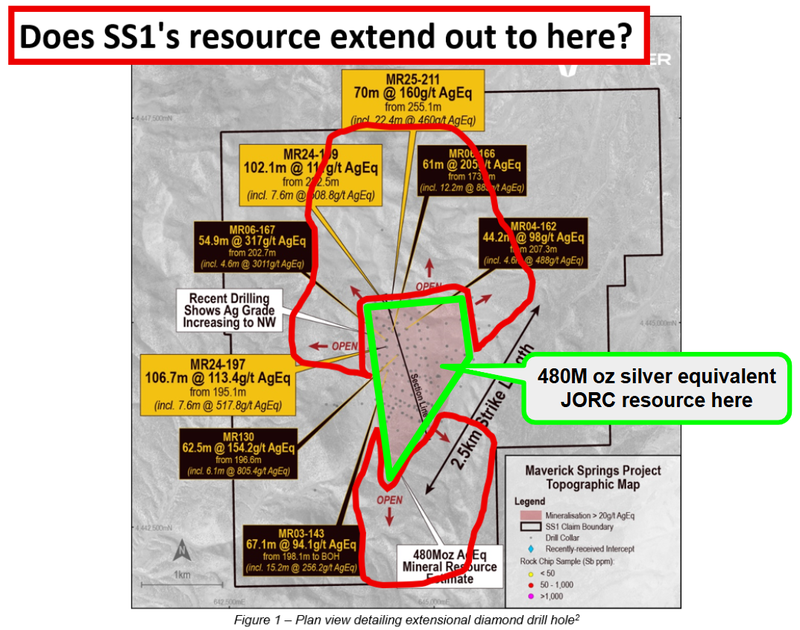

SS1 has a 480 million ounces of silver equivalent JORC resource estimate on one asset in Nevada, USA.

SS1 is drilling right now to grow that resource even further, and lately has been hitting high grade silver at shallower depths than the existing resource estimate.

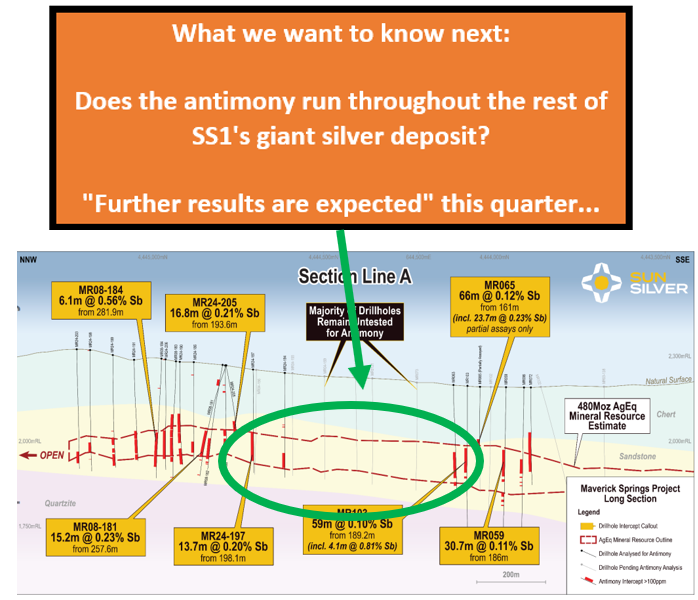

SS1’s project could ALSO host a giant antimony deposit - previous drilling on the project had never been assayed for antimony.

SS1’s resampling of old core (and the results from the new holes being drilled) keep showing antimony - and we know how that there is antimony mineralisation across two parts of SS1’s giant silver deposit:

(Source)

SS1 is aiming for a silver resource estimate upgrade AND potentially a maiden antimony resource estimate before the end of the year.

Antimony is a US critical military metal and after Chinese export restrictions in late 2024 - the price of antimony has gone up more than 300%.

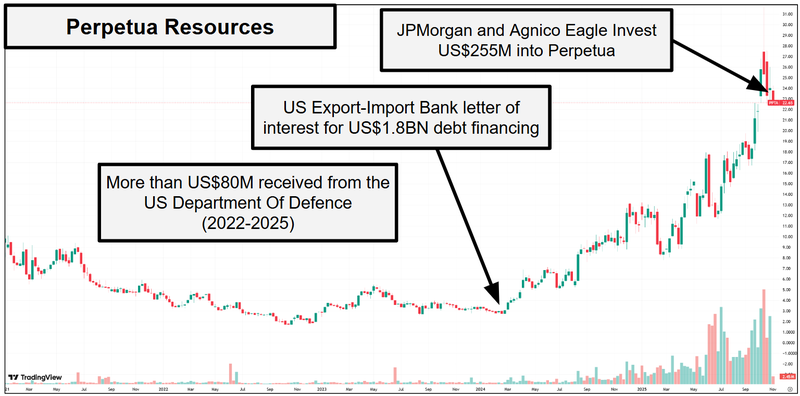

Those export restrictions have triggered a rush by the US government into backing projects with antimony resources’ - the biggest company being Perpetua Resources.

Perpetua has gone from a market cap of ~$200M to now trade at ~$4.5BN after the US government has given the company close to US$2BN in grants and debt funding support.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

Perpetua is now officially developing its project.

We think there are similarities between Perpetua and SS1…

Perpetua’s main asset is a primary gold project, with a giant antimony resource that is hosted alongside the gold.

SS1’s main asset is a primary silver project, which COULD potentially host a giant antimony resource (which we think could rival Perpetua’s)...

Perpetua’s antimony resource is the biggest defined antimony resource in the US right now and we think there is a chance SS1’s project ends up with a bigger defined resource estimate because:

- SS1 is hitting grades at or above Perpetua Resources’ average antimony grade of 0.07% - SS1’s last two holes returned antimony grades averaging 0.1% and 0.12%.

- SS1’s project is ~67% bigger than Perpetua’s in terms of tonnage - Perpetua’s antimony resource is based on 132.2mt of material at 0.07% antimony grades. SS1’s silver resource is based on 221Mt of material... 221Mt, even at the same grades as Perpetua would give SS1’s project a much bigger antimony resource.

With the US considering adding silver to its critical minerals list - we think SS1’s deposits (once an antimony resource is defined) could have strategic value inside US borders.

And we think a giant antimony resource could be what starts to unlock government funding support…

Government funding could be what unlocks SS1’s project

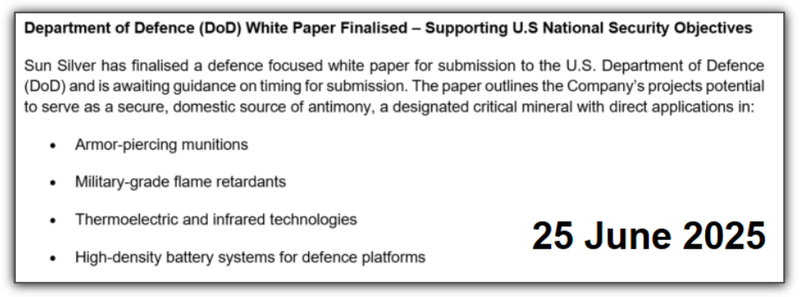

SS1 recently finalised a white paper to submit to the Department of Defence (DoD) for funding.

(Source)

And we note that SS1 has explicitly said that it was pursuing US DoD funding right now…

(Source)

Why is that important?

Because we think government funding could ultimately be what unlocks SS1’s giant silver resource.

SS1’s silver deposit starts from ~200m underground - which is considered relatively deep.

Yes, an estimated 480M ounces is a LOT of silver, but SS1 needs to dig a big expensive hole (pit) to reach it before they can extract and sell it.

That pre-strip (digging down to the juicy valuable bits of the project) means a lot of upfront capital spend which is typically where project financiers get scared off a project.

Conventional project financiers (and equity investors) want as fast a payback as possible with mining projects, big CAPEX upfront can scare off these investors.

As the silver price goes higher that pre-strip matters less and less.

BUT government funding or some sort of government-backed loan could be what really unlocks SS1’s project.

Exactly the same way it did for Perpetua’s project in Idaho.

Perpetua received commitments for a US$1.8BN loan from US Export-Import Bank and then private capital started pouring into the company in a big way.

Perpetua's market cap has gone from $300M to $4.5BN.

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

We think a similar re-rate could happen to SS1 if the government was to backstop its project with some sort of funding deal.

We aren’t the only ones either…

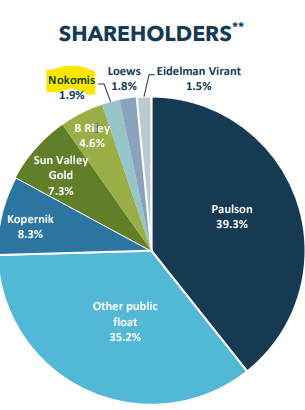

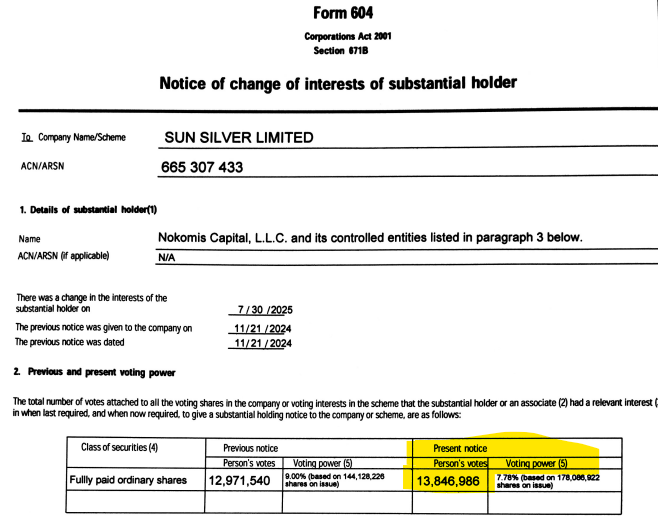

We have already seen one of the early backers of Perpetua Resources (Nokomis) take a big shareholding in SS1.

Here is Nokomis listed as a major shareholder of Perpetua from a presentation back in 2023:

(Source)

Nokomis is now one of SS1’s biggest shareholders (holding 7.79% of the company).

And we noticed they increased their position in the most recent capital raise.

(SS1 just raised $30M and now has ~$34M cash in the bank)

(Source)

SS1 has just listed in the US - which might help with government engagement…

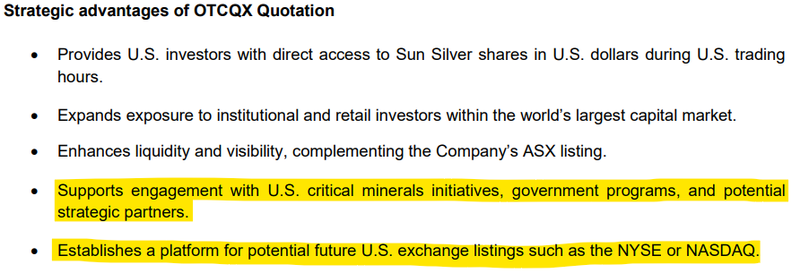

SS1 has just announced its US OTC listing... ahead of a potential future listing on a bigger exchange like the NYSE.

The listing is on the OTCQX which is the highest tier of the OTC, with stricter and higher standards.

This move will allow direct access to capital from US based investors and will allow SS1 to gain a more prominent presence within the US.

The aim of this will be to leverage off this to seek out opportunities (government or strategic partners) to help progress the project into development and production.

It was also stated in the announcement the intention to list on other US exchanges such as the NYSE or NASDAQ.

(Source)

A US listing could also boost SS1’s chances of getting US government funding/support.

US public support for a company with a US listing could be stronger as opposed to SS1 only being listed in Australia.

That could also mean there is public support for the project from shareholders who buy over there.

See our deep dive on why we think a US listing would be good for SS1 here.

6 ingredients that worked for VUL - will they work for SS1?

SS1 reminds us a lot of the early days of one of our best ever Investments Vulcan Energy Resources (ASX: VUL).

At its peak VUL was up 8,225% from our Initial Entry Price.

We are hoping that SS1 is shaping up to do something similar to VUL - we just need the silver and antimony macro themes to behave, which unfortunately no one can control.

The main reason VUL was able to run as hard as it did was because the lithium price went parabolic in 2021-2022.

Which meant the market was willing to re-rate material news that VUL put out.

Now we just need SS1 to deliver the news it says it will…

AND for silver and antimony prices to run to levels higher than the market expects.

Any increase in the silver price matters a lot for SS1 because of how big its resource is…

You can do your own maths on what every incremental increase of US$1 per ounce in the silver price means for the potential in ground value of SS1’s 480 million ounce silver equivalent resource estimate.

Of course continued uptrend of the silver price is no guarantee to continue.

A few weeks back we put out a note going through the “6 ingredients” SS1 will need to create the same tailwinds for a VUL style run”.

Read that full note here where we go through how SS1 ranks across those six ingredients:

- Acquired the project in a down cycle - SS1 picked up its silver project in August 2023 when the price was low and interest in silver was minimal.

- Project size and scale is big - SS1 now has the largest pre-production silver asset on the ASX and in the USA, with growing resources (and a possibly antimony resource)

- In an emerging hot theme - For VUL it was battery metals and lithium. For SS1 it is the booming US precious/critical metals theme, thanks to its silver and antimony potential.

- In a country with demand for the end product - Located in Nevada USA, which is a key region for domestic critical minerals supply.

- Be the first mover - SS1 IPO’d early in 2024, ahead of the silver and antimony price runs.

- Then wait for that commodity price run.... - Silver and antimony prices have already had a bit of a run.

You can read more about these “ingredients” here: The final ingredient SS1 needs in our "recipe for an 8,000% VUL style price run"... but ingredient #6 is the hardest one to get…

Sun Silver

ASX: SS1

We have been Invested in SS1 for over 18 months now:

Since then, we have followed and written about SS1 as the company’s story has evolved.

Here is a list of some of the biggest developments for SS1 over that period - basically this is an archive of SS1’s “best hits” and our take on them:

- SS1 is now the biggest primary silver resource on the ASX

- SS1 is leveraged to the silver price

- Silver to be classified as a critical mineral in the USA?

- Nevada is the “Silver State”, with mines everywhere

- How does SS1’s project rank against some of the other mines in the region?

- From a technical/charting perspective, the momentum is in silver’s favour as well…

- Silver M&A a precursor to a big run in the silver price?

- Silver Squeeze coming?

- Eric Sprott’s silver Exchange Traded Fund (ETF) is buying SS1

- SS1 is also going for downstream value-add opportunities

- SS1’s project could also host a giant antimony resource

- Why an antimony resource could be a game-changer for SS1

- Perpetua Resources - Can one company deliver the US all its antimony needs?

- SS1’s giant silver deposit could be mineralised from surface…

- SS1 is headed for a US stock exchange

- SS1 just raised $30M - led by global institutions

Sun Silver:

ASX: SS1

10 Reasons we are Invested in SS1

The below reasons are from our latest SS1 Investment Memo (published 26 of March 2025).

Since then, a fair bit has changed in the markets, so we have included updates below each reason:

1. SS1 has the largest primary silver resource on the ASX

SS1 has a 480M ounce silver equivalent JORC resource estimate.

This is the largest pre-production primary resource on the ASX.

There is a premium attached to being the “biggest” of any commodity in a particular market and funds or investors wanting leverage to silver (without buying the commodity itself) will ideally look to SS1 first.

2. SS1 is extremely leveraged to movements in the price of silver

Silver is generally produced as a by-product from producing base metals. But because SS1 is a primary silver producer, it means that for every US$1 per ounce that silver increases, it has a material increase on the in-ground value of SS1’s project.

This has the effect of SS1’s share price generally tracking very closely to the price of silver.

If silver goes up (and goes up in a big way) then so too should SS1.

🚨Update:

Silver recently hit all time highs at $54/oz and has been hovering near US$50/oz, currently still up around US$25 per ounce (~100%) from when we published our last SS1 Investment Memo.

Every time the silver price goes up, the in-ground value of SS1’s 480M silver equivalent JORC resource estimate increases.

3. We are bullish on silver and the price is reaching decade highs

The silver price is re-testing a 12 year high at the time of writing (around US$34/oz) as silver demand is fast outstripping supply.

We think the long term macro tailwinds for silver are incredibly strong and should help SS1 as it looks to take its resource into development.

🚨 Update:

Silver is up around 100% since we launched our latest SS1 Investment Memo.

Silver is also up over 100% since SS1 first picked up its project:

(Source)

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

4. SS1 is reaching a size where it could potentially be included in index funds

SS1 is currently capped at ~$103M. It is reaching a size and liquidity profile where it could qualify for inclusion in the ASX indices.

Getting into an index opens up SS1 to a whole new pool of capital and it makes the company a potential investment opportunity for institutional investment funds.

If SS1 gets into an index like the ASX All Ords it could become the de-facto ASX Silver ETF and the only way for passive funds to get leveraged silver pre-production silver exposure on the ASX.

🚨 Update:

SS1 just completed a $30M capital raise and is currently capped at $125M.

We have said previously that the $150-200M range is where SS1’s project will start to enter that “index inclusion territory”.

Since the middle of this year we have seen the Sprott Silver ETF start buying SS1 shares… (hopefully the first of many indexes/ETF’s).

See our index inclusion thesis here: SS1 index inclusion upside - the only way to get silver exposure on the ASX...

5. The US Department of Defence wants antimony, SS1 may have it

The US imports 90% of its antimony which all come from potentially hostile countries (China, Russia and Tajikistan) and it has no antimony production of its own.

Antimony is a critical mineral for various military applications including as a hardening agent for ammunition.

SS1 has identified antimony across its project from xPRF analysis and drilling data collected in 2024.

🚨 Update:

The US government has started Investing directly into critical minerals projects inside the US.

We have seen the Pentagon take a direct stake in MP Materials.

The US government also took a 5% stake in Lithium America’s…

We think the government funding available for critical mineral resources just keeps growing.

6. Can SS1 be the next $4.5BN capped Perpetua Resources?

Perpetua Resources has a gold-antimony resource in Idaho, USA.

The US Government, through the Department of Defence, has provided over $50M in grants as well as a $1.8BN loan to help fund the development of the mine.

The US Government was particularly interested in the antimony potential of that project.

We think that if SS1 is able to develop a US-based antimony resource it could also be supported by the US Government - like Perpetua Resources.

🚨 Update:

IF SS1 can define an economic antimony resource across its project we think it could become a sort of Perpetua 2.0.

SS1 is currently capped at ~$180M, Perpetua is capped at A$4.5BN.

Interestingly, early backers of Perpetua (Nokomis Capital) are also one of SS1’s biggest shareholders (Nokomis owns 7.79% of SS1)…

Perpetua was also the first company to get investment from JP Morgan as part of its US$1.5 Trillion push into critical US industries AND it attracted a strategic investment from Agnico Eagle - the world’s 3rd bigget gold miner.

Check out our side by side comparisons of SS1 and Perpetua here: Is antimony going to be the dark horse for SS1 in 2025?

7. SS1 has a Carlin-Style deposit, cheap and easy to mine.

SS1’s project is located in the “Carlin Trend”, an area that is home to some of the biggest gold and silver mines in the world.

In the mid-1980s Barrick made a Carlin-Type discovery at its “Goldstrike” project in Nevada (not too far from SS1).

This was the project that put the company on the map and produced around 200,000 ounces at 1.2g/t of gold and 200,000 ounces of silver in the mid-1990s.

What made this project so successful was that it was a low cost mining production.

If SS1 can prove that it can extract the gold and silver from its resource with a similar process used by Barick on its Goldstrike Project it could have a material impact on the feasibility of SS1's project.

🚨 Update:

In a previous SS1 note we did a deep dive on Carlin style deposits and why they are able to operate profitably with low costs.

Check out our deep dive into how SS1’s project compares to $9BN Coeur Mining’s Rochester project here: How does SS1’s project rank against some of the other mines in the region?

8. SS1 is in Nevada USA, near some of the best gold and silver mines in the world.

Nevada is a big mining state and the area of Nevada that SS1 is working in is called Elko County.

There are major gold and silver mines scattered throughout this area of Nevada, and Elko County is very familiar with the mining industry.

$45BN Barrick and $14BN Kinross both own projects in the region.

This means that there is a high level of skilled labour in the area and permitting processes are well known.

9. JORC resource includes ~2.16M ounces of gold

Included inside SS1’s 480m ounce silver equivalent JORC resource is a ~2.16M ounce gold resource.

With the gold price also at record highs, the in-ground value of SS1’s project is also leveraged to the increase in the price of gold.

10. Downstream value add: “Silver paste” production (for solar) could improve economics

SS1 has a giant silver resource within the US. Silver is a key material used in solar panels in the form of silver paste.

SS1 is evaluating the merits of developing downstream silver paste processing.

The world’s solar manufacturing capacity (including silver paste production) is heavily concentrated in China. If SS1 is able to produce silver paste in the US this could add to the merits of the project.

🚨 Update:

A big part of our long term investment thesis for SS1 is that its silver could be used downstream to produce silver paste that goes into solar panels.

Check out our deep dive on SS1’s silver paste angle here: Silver Squeeze coming?

Ultimately, we are hoping a combination of the above reasons help SS1 achieve our Big Bet which is as follows:

Our SS1 Big Bet:

“SS1 re-rates to a +$300M market cap by expanding its large US silver resource and moving into development studies and/or attracting a takeover bid at multiples of our Initial Entry Price”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including development risk, country risk and commodity price risk - just some of which we list in our SS1 Investment Memo.

Success will require a significant amount of luck. Past performance is not an indicator of future performance.

What are the risks?

In the short term we think the key risk for SS1 is “Commodity price risk”.

There is commodity price risk, because SS1’s share price tends to move up and down with the silver price.

Silver is currently battling a breakout above that US$50 level where it has historically failed to convincingly clear without selling.

There is always a risk history repeats itself and the silver price comes down from here.

IF the silver price was to fall, we would expect to see weakness in SS1’s share price.

Commodity price risk

The performance of commodity stocks are often closely linked to the value of the underlying commodities they are seeking to extract. Should silver and gold prices fall, this could hurt the SS1 share price.

Source: “What could go wrong?” - SS1 Investment Memo 26 March 2025

Other risks

Like any stock market investment, investing in SS1 carries a range of risks which may affect the value of the company, some of which cannot be predicted (this is the nature of risks).

Here we aim to identify a few more risks.

SS1’s Maverick Springs Project in Nevada is a large pre-development silver project that is not yet producing. There is a risk that the project does not progress to production or that development takes longer and costs more than expected.

SS1’s share price is highly leveraged to the price of silver. A sustained decline in silver, or gold, could materially impact project economics and investor sentiment.

The company may also be exposed to volatility around the classification of silver as a US critical mineral. While inclusion could bring upside, there is no guarantee it will occur.

SS1 remains reliant on the capital markets to fund exploration and development activities. Any future equity raisings could dilute existing shareholders, while debt funding may not be available on favourable terms.

Although SS1’s project is located in a stable jurisdiction, permitting, environmental approvals, and local regulatory processes can still present delays or uncertainties.

The company’s valuation has risen significantly in recent months, meaning the current share price may already reflect some of the expected future upside.

Finally, while US government support or funding could act as a major catalyst, there is no certainty that such assistance will be provided.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our SS1 Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing.

We use this memo to track the progress of all our Investments over time.

Click here to read our SS1 Investment Memo where you will find:

- What does SS1 do?

- The macro theme for SS1

- Our SS1 Big Bet

- What we want to see SS1 achieve

- Why we are Invested in SS1

- The key risks to our Investment Thesis

- Our Investment Plan